Stop Selling Your Crypto. Here Is How a Credit Line Gives You the Cash You Need Without Losing Your Position.

You need cash. Your crypto portfolio is sitting on significant gains. Selling feels like the obvious move, but the moment you do, you trigger a taxable event, you lose your position, and if the market runs higher next week, you are left watching from the sidelines.

That tension is real in 2026. According to a 2025 report by the Financial Stability Board, retail crypto holders globally are sitting on an estimated $2.3 trillion in digital assets, yet liquidity access remains a persistent friction point for individuals who do not want to exit their positions. The need for a smarter solution has never been more obvious.

Clapp's credit line model answers that need directly. It lets you use your crypto as collateral, borrow against it, and stay fully invested at the same time. This article breaks down exactly how it works, why it matters, and what you need to know before you use it.

Key Takeaways

- You can access liquidity from your crypto holdings without triggering a sale or a capital gains event.

- Clapp supports 19 different cryptocurrencies as collateral on a single, flexible credit line.

- You can swap your collateral for a different asset without closing or restarting your credit line.

- Loan-to-Value (LTV) ratios, liquidation thresholds, and collateral health must be actively managed to protect your position.

What Is a Crypto-Backed Credit Line and How Does It Work? The Mechanics You Need to Know First.

A crypto-backed credit line is a revolving borrowing facility where you deposit cryptocurrency as collateral and receive access to a credit limit in fiat or stablecoins, without selling your underlying asset.

Think of it like a home equity line of credit, but your house is Bitcoin, Ethereum, or one of 17 other supported assets on Clapp's platform. You lock your crypto in a smart contract or custodial vault, and the platform extends you a credit limit based on a percentage of that collateral's current market value.

How the Credit Limit Is Calculated?

The core ratio is called the Loan-to-Value ratio, or LTV. If you deposit $10,000 worth of Bitcoin and the platform offers a 50% LTV, you can borrow up to $5,000.

The LTV varies by asset. More volatile assets typically carry lower LTV ratios because the platform needs a larger buffer to protect against sudden price drops. Clapp applies tiered LTV caps that reflect the risk profile of each of its 19 supported collateral assets.

The Role of the Smart Contract

On-chain credit line protocols use smart contracts to hold collateral in escrow. The contract monitors the real-time value of your collateral. If that value drops toward a liquidation threshold, the contract triggers automatic warnings or, in some cases, automatic partial liquidation to protect the lender.

This is not optional. It is baked into the protocol at the code level.

What Happens When You Repay?

Repayment is flexible on a revolving credit model. You can repay in full, repay partially, or make interest-only payments depending on the product structure. Once you repay the borrowed amount, your collateral is released back to you.

Is It Better to Borrow Against Crypto or Sell It? A Straight Comparison That Most Platforms Avoid.

In most cases, borrowing against appreciating crypto assets is more financially efficient than selling, because it avoids capital gains tax, preserves your market exposure, and keeps your long-term investment thesis intact.

This is not a blanket rule. It depends on your situation. But for holders who believe in the long-term value of their assets, selling to access short-term liquidity is often the most expensive option.

The Tax Argument

In most jurisdictions, selling cryptocurrency is a taxable disposal event. A 2025 analysis by PricewaterhouseCoopers covering 40 countries found that the average effective capital gains tax rate on crypto disposals for retail investors sits between 15% and 30% depending on the holding period and local legislation.

Borrowing against your crypto is not a disposal. You still own the asset. The loan proceeds are not income. This distinction can represent thousands of dollars in preserved wealth for a mid-sized holder.

The Opportunity Cost Argument

If you sell Bitcoin at $80,000 to cover a $20,000 expense and Bitcoin reaches $120,000 six months later, you have lost the upside on the 0.25 BTC you sold. That is $10,000 of missed appreciation that a credit line would have let you keep.

When Selling Actually Makes More Sense?

There are scenarios where selling is the right call. If you are at a loss and want to harvest that loss for tax purposes, selling makes sense. If the interest rate on your credit line exceeds the expected appreciation of your collateral, selling is cheaper. Always model both scenarios with your specific numbers before deciding.

What Cryptocurrencies Can Be Used as Collateral? Why 19 Supported Assets Is a Structural Advantage.

Clapp supports 19 cryptocurrencies as eligible collateral on a single credit line, which is significantly broader than the industry standard of 2 to 5 assets offered by most competing platforms.

This is not a marketing detail. It changes the practical utility of the product in meaningful ways.

Comparing Collateral Support Across Platforms

| Platform | Supported Collateral Assets | Multi-Collateral in One Line | Collateral Swap Without Closing |

|---|---|---|---|

| Clapp | 19 | Yes | Yes |

| Aave (v3) | ~10 (per market) | Yes (per pool) | Limited |

| MakerDAO | ~10 vault types | No (separate vaults) | No |

| Traditional Crypto Lenders | 2 to 5 | Rarely | No |

Source: Platform documentation as of Q1 2026. Subject to change.

Clapp Glossary: Compound Interest 📚

— Clapp Finance (@ClappFinance) February 24, 2026

💡Compound interest — for instance, on crypto savings — makes your money work overtime to make even more money.

Unlike simple interest that only pays you on the original deposit, it adds your previous earnings to the pile — so the next time… pic.twitter.com/GpQ8pNbmzm

Why Multi-Collateral Matters in Practice

Imagine you hold a diversified portfolio: Bitcoin, Ethereum, Solana, and a few altcoins. Most platforms force you to open separate vaults or accounts for each asset. That means separate liquidation thresholds, separate repayment schedules, and separate monitoring overhead.

Clapp consolidates all 19 supported assets into one credit line. You have one interface, one balance, one set of terms to track.

The Diversification Buffer Effect

When your collateral is spread across multiple assets, their price movements are not perfectly correlated. A drop in Solana might not coincide with a drop in Bitcoin. A multi-collateral structure means the aggregate health of your collateral position is more stable than any single asset would be alone. This reduces the frequency and severity of margin call scenarios.

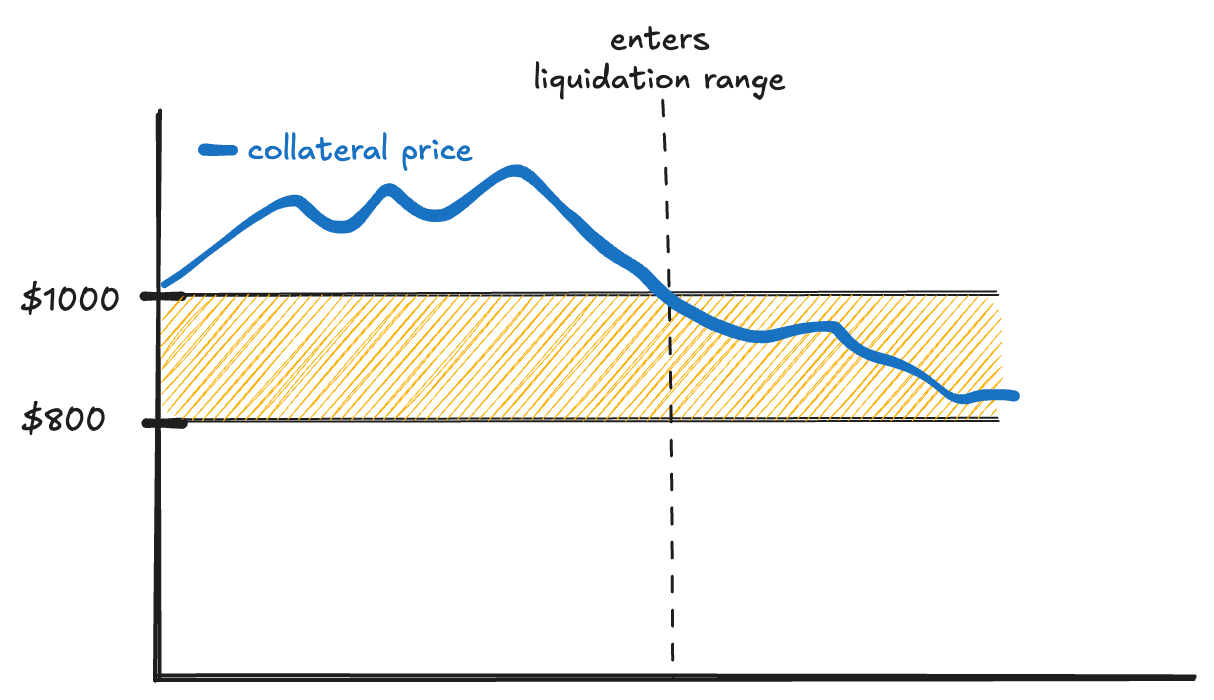

What Happens to My Crypto Collateral If the Market Drops? Understanding Liquidation Before It Happens to You.

If the value of your collateral falls below the platform's defined liquidation threshold, Clapp will begin a liquidation process that sells a portion of your collateral to bring the LTV ratio back within acceptable bounds.

Understanding this mechanism is not optional. It is the most important risk factor in the entire model.

How Liquidation Thresholds Work

Every credit line has two critical numbers: the maximum LTV (the limit at which you can borrow) and the liquidation LTV (the point at which automatic liquidation begins).

For example, if your maximum LTV is 50% and your liquidation LTV is 75%, you have a buffer. If your $10,000 collateral drops in value to $6,667 while you still owe $5,000, your real LTV is now 75% and liquidation begins.

The Warning System

Clapp issues health factor alerts as your LTV approaches the liquidation threshold. These alerts give you time to either add more collateral, repay part of the loan, or swap your collateral into a more stable asset.

How to Protect Yourself?

There are three practical defenses against liquidation. First, borrow conservatively. Starting at 30% to 40% LTV gives you substantial room before reaching the liquidation threshold. Second, monitor your position during periods of high market volatility. Third, keep reserve assets available that you can add to your collateral position quickly if needed.

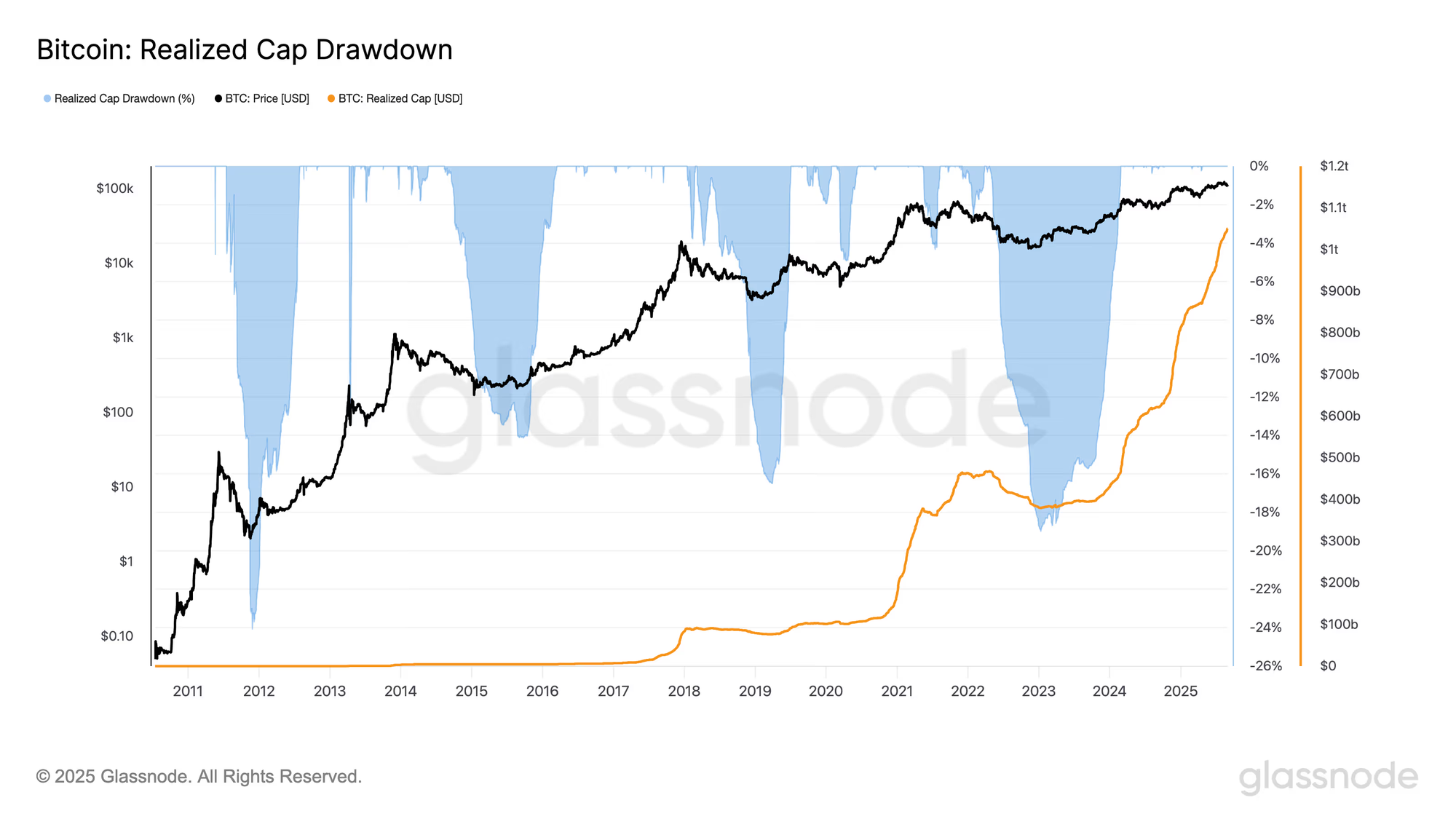

Historical Context on Crypto Drawdowns

According to data published by Glassnode in their 2025 annual on-chain report, Bitcoin has experienced intra-year peak-to-trough drawdowns of 30% or more in six of the last ten calendar years. Any credit line user must treat a 30% to 50% drawdown as a realistic planning scenario, not a worst-case outlier.

How Do I Swap Collateral Without Closing My Credit Line? The Feature That Changes Everything.

Clapp allows users to replace their deposited collateral with a different supported asset while keeping the credit line active, the borrowed balance intact, and the account in good standing, without any interruption to the facility.

This feature has no direct equivalent in most traditional crypto lending products. It is worth spending real time understanding why it matters.

The Problem It Solves

Markets shift. The asset you used as collateral six months ago may now look overextended. You might want to rotate into a different asset that you believe has stronger near-term support, or you might want to reduce exposure to a volatile asset before a major macroeconomic event.

Without a collateral swap feature, your only option is to repay the entire loan, retrieve your collateral, sell it, buy the new asset, and re-open the credit line. That process takes time, incurs multiple transaction fees, and potentially triggers taxable events at each step.

How the Swap Works on Clapp

The collateral swap mechanism is executed through the platform's interface in a coordinated transaction. The new collateral asset is deposited, the outgoing collateral is released, and the credit line health factor is recalculated using the new collateral's LTV parameters. The borrowed balance stays exactly where it is.

Strategic Uses of Collateral Swapping

A user who entered a credit line using Ethereum as collateral during a period of high ETH prices can, if they believe ETH is about to correct, swap that collateral for Bitcoin or a stablecoin-supported collateral tier. They retain their borrowed liquidity. They restructure their underlying risk. They do it in one step.

This is active treasury management for individual crypto holders. It is a feature set that was previously only accessible to institutional desks with custom over-the-counter agreements.

Why the "Borrow, Not Sell" Philosophy Is More Than a Tagline: The Economics Behind It.

The phrase "why sell when you can borrow" is more than positioning. It reflects a specific and defensible set of assumptions about crypto as an asset class in 2026.

The Long-Term Appreciation Thesis

The underlying assumption is that the assets used as collateral will appreciate over the medium to long term. If that assumption holds, and the interest cost of the credit line is lower than the appreciation rate of the collateral, the math favors borrowing every time.

Interest Rate Comparisons

According to a 2026 DeFi market survey published by Messari, the average annualized borrowing rate on crypto-backed credit facilities ranged from 5% to 12% depending on the asset and platform, compared to average unsecured personal loan rates of 18% to 24% in the same period.

For a holder with strong collateral and responsible LTV management, a crypto credit line is among the cheapest forms of accessible liquidity available.

The Psychological Dividend

There is also a behavioral component. Selling an asset that has appreciated significantly triggers a psychological sense of loss among long-term believers in that asset. The credit line model removes that friction entirely. You access the cash. You keep the crypto. The cognitive load of "did I sell too early?" disappears from the equation.

What Does the Future Hold? Where Crypto Credit Lines Are Heading Over the Next Three Years.

The infrastructure supporting crypto-backed credit is maturing rapidly, and the next 36 months are likely to produce changes that make the current model look like an early version.

Regulatory Clarity Is Coming

The European Banking Authority published guidance in late 2025 that began classifying crypto-backed lending under a formal risk framework for the first time. The Financial Stability Board released a parallel report recommending that G20 nations establish specific capital adequacy rules for platforms offering crypto credit. This regulatory clarity, while adding compliance overhead, will ultimately legitimize the sector and open it to a broader institutional audience.

Cross-Chain Collateral

Current platforms, including Clapp, primarily operate within specific blockchain ecosystems. The next evolution is cross-chain collateral, where assets on Ethereum, Solana, Bitcoin Layer 2 networks, and others can all be pledged simultaneously through interoperability protocols like LayerZero and Chainlink CCIP. Early pilots were live by mid-2025, and full production deployment is expected across leading platforms by 2027.

AI-Driven Risk Management

Several platforms were piloting AI-powered liquidation prevention systems in 2025 and 2026, designed to automatically rebalance collateral positions in real time based on predictive volatility models. This moves the risk management burden away from the user and toward the protocol itself, which could significantly reduce liquidation events across the industry.

Institutional Adoption

Goldman Sachs Digital Assets and several European private banks had begun exploring crypto credit lines as a complement to traditional securities-backed lending programs by Q4 2025. As custody infrastructure improves and regulatory frameworks solidify, institutional adoption is widely expected to accelerate through 2027.

The Smartest Move You Can Make With Your Portfolio Starts Here.

You now have the full picture. Crypto credit lines are not a workaround or a loophole. They are a mature financial instrument designed for people who have conviction in their assets and need access to capital without abandoning that conviction.

Clapp's model advances this by combining 19-asset collateral support, a flexible revolving credit structure, and the ability to swap collateral without closing your line, all in a single product.

If you hold crypto and have never modeled what a credit line against your portfolio could do for you, today is the day to run those numbers.

Open Clapp's credit line calculator, input your current holdings, and see your borrowing capacity in under two minutes.

Quick Win for Beginners

One concrete first step you can take today: Calculate your current portfolio value and apply the 40% LTV rule. That is a conservative estimate of what you could borrow against your holdings without approaching liquidation risk. Write that number down.

One resource suggestion: Read the Financial Stability Board's 2025 crypto lending risk report. It is publicly available and gives you a clear understanding of how regulators view this space, which helps you assess platform risk intelligently.

One question to sit with: If you had access to 40% of your portfolio value as a credit line right now, what financial goal would you use it to achieve first?

Disclaimer: This article is for educational and informational purposes only. Nothing in this content constitutes financial, tax, legal, or investment advice. Crypto-backed lending involves significant risk, including the potential loss of collateral through liquidation. Market conditions can change rapidly and without warning. Readers should conduct their own due diligence and consult a qualified financial advisor, tax professional, or legal counsel before making any borrowing or investment decisions. Clapp and all platform features referenced are subject to their current terms of service and eligibility requirements.